Increasing Complexity & Growing Markets Should Benefit Liberty Tax

Benjamin Franklin and others have reminded us that nothing is certain in life except death and taxes. As a result, it would seem that these two certainties would lead to interesting

and enduring business opportunities. For this article, I will concentrate on the taxes side and how a small company named Liberty Tax (NASDAQ:TAX) makes for an interesting opportunity in this unfortunately perpetual industry. Hopefully I and Liberty Tax can make you feel a little bit better about April 15 th, and also make you conclude that taxes don't have to always take money out of your pocket but can put money into it. Let's begin.

Stand Out From The Crowd

You might have seen people like those in the picture above dressed up as Lady Liberty and a little too enthusiastic about taxes than maybe one, two, or a dozen people should be. These people are hard at work though trying to make enough to pay their own taxes and are a part of Liberty Tax's guerilla marketing campaign. In addition to the enthusiastic attention-grabbing tactics, Liberty expands its brand by hosting community events, parties, and educational events at day care centers. Liberty strives to get its name out there in a fun way and makes a concerted effort to market itself as a people -focused tax preparer as opposed to a corporate one like H&R Block (NYSE:HRB). I think this is important as getting your taxes done can be a laborious, impersonal process, but a bill or refund can mean a lot to a family looking to get a new car, move into a bigger house, or simply just keep its standard of living. So Liberty's embracing marketing should benefit the company going forward and make it stand out in an inherently dull industry.

A Growing (& Growing More Complicated) Market

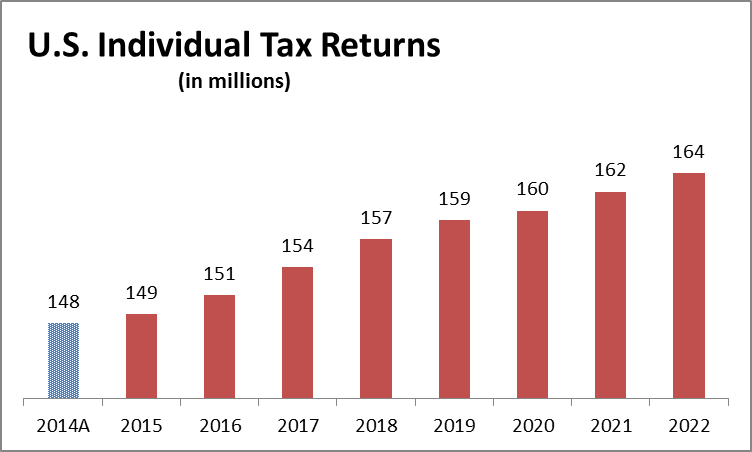

The number of taxpayers has grown and is estimated to keep growing, albeit at a relatively slow pace: 1.4% on a compounding basis from now until 2022. (I used the 2015 estimated figure in the chart below as the base year.)

Click to enlarge

Click to enlarge

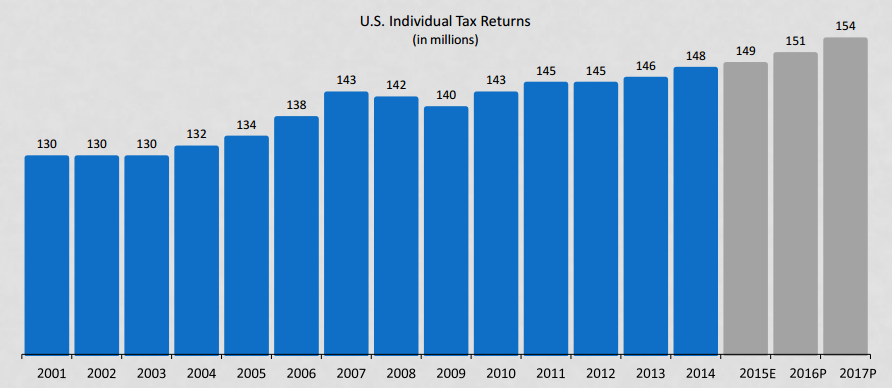

Although the 1.4% growth rate may seem relatively miniscule, it is also relatively more reliable given the recession resistant nature of the tax industry. Recessions and financial crises don't let taxpayers off the hook. Fairly small drops can be seen in the recession years of 2008 and 2009, but 2010 equals 2007 and then tax returns continue to grow. This can be seen in the following chart of the number of tax returns in years past:

Click to enlarge

Click to enlarge

Source: Liberty Tax Presentation (attached)

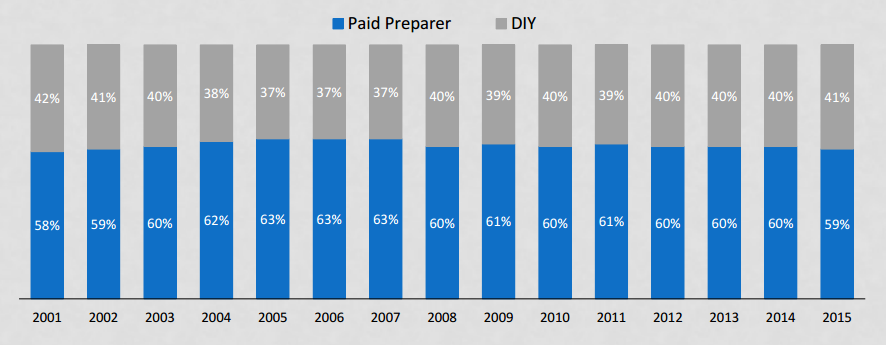

What surprised me about the tax preparation market is that consumers are not increasingly doing their own taxes on a percentage basis. This is true even with the advent of electronic means of doing your taxes with software from the likes of H&R Block, Intuit (NASDAQ:INTU), and Liberty itself. Software, supposed to make filing easier, and online providers have not eaten into the paid preparer market. It seems as if the do-it-yourself (DIY) tax filers are just switching to electronic means of filing in lieu of pen and paper - but those electronic means have not propelled filers to switch from paid preparers to DIY. This is good news for Liberty:

Click to enlarge

Click to enlarge

Source: Liberty Tax Presentation (attached)

It seems as if taxpayers still value the services of tax preparers and are not eager to become tax preparers themselves. Liberty points out in its presentation that people value independence and the opportunity cost of not doing their taxes does not outweigh the benefits of doing something else whether it be work or play. Liberty points out that revenue is growing in various industries that entail activities that could otherwise be done by their customers. These industries include landscaping, pet care, beauty, and cleaning. Nail salon revenue grew 34% from 2010 to 2013 and Molly Maid, a cleaning service, had projected revenue growth of 20%. So surely an industry requiring more esoteric knowledge like tax preparation would not invite lay people to increasingly partake in DIY. This will benefit Liberty, its franchisers, and its investors.

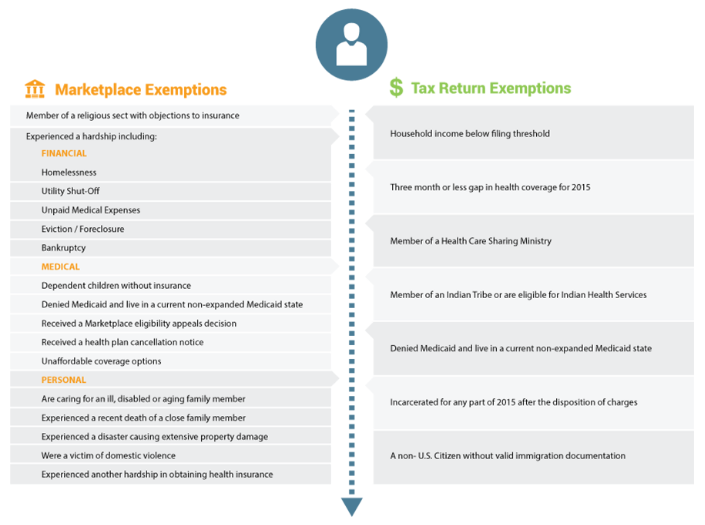

Not only will the number of tax filers grow, but the filing of taxes will grow more complicated as the Affordable Care Act (ACA), colloquially known as Obamacare, gets implemented further. The ACA will create an increased need for tax preparers who know how to file with the new penalties and forms brought on by the ACA. Employees will have to deal with 1095 forms in order to report their health insurance coverage and need knowledgeable preparers to interpret them and transcribe the information onto their returns. Further, the tax penalties for not having insurance are increasing mightily in 2016 compared to 2015. Liberty's tax preparers can help tax payers not only understand the increased fees and why they are assessed but also the exemptions that may apply to them in order to avoid them.

Tax payers without insurance are required to pay a flat fee or a percentage of their income, whichever is higher. The flat fee penalty is more than doubling and so is the maximum penalty under that flat fee. If higher, the penalty as a percentage of their income will be 2.5% in 2016 compared to 2% in 2015. The structure is characterized as follows:

These steep increases in the penalties for not having insurance only add importance to having a tax preparer who understands the penalties and the associated forms. The exemptions under the ACA are numerous as well and preparers can help filers navigate them:

Click to enlarge

Click to enlarge

The Uber of Tax Preparation

Liberty Tax can be similar to Uber by helping people take on a new job fairly quickly and offering people a flexible mode of employment. The seasonality of the tax industry lends itself to temporary work and so franchisers and employees of those franchises and company-owned offices can use Liberty as a vehicle for extra income like Uber, while still partaking in other employment and leisure activity. In fact, 2/3 of Liberty's franchisees have other jobs. You don't have to be an accountant or CPA to thrive with Liberty because it is fundamentally not trying to target businesses or individual taxpayers with extremely complicated returns.

Liberty is already the second largest tax preparer in the U.S. and Canada with about 4,500 offices. Liberty also maintains an asset-lite business model with over 95% of its Liberty locations franchised. By keeping its offices mostly owned by franchisees, Liberty engenders the pride of ownership and helps franchisees partake in the upside of the tax preparation market and not have their compensation stagnate. Further, Liberty helps entrepreneurs capture the benefits of being an independent tax preparer with the aid of a larger corporate partner without all the downsides. Liberty offers financial products that you might expect from a larger preparer like H&R Block such as refund transfers, refund advances, and debit cards to build an enduring relationship with Liberty that extends past tax time. U.S customers utilize Liberty's financial products about 50% of the time and they are a growing source of revenue for the company as we'll see later.

The increasing complexity of tax filings combined with the enduring nature of the industry gives prospective franchisers a good business with fairly predictable demand. People are going to have to file their taxes; you just have to go out there like Liberty does with its guerilla marketing campaigns and let tax filers know that you're there and offer a differentiated and better experience. The capital requirements to open a Liberty franchise are fairly low at around $65,000 and the overhead is low with its seasonal nature - an office doesn't have to be at full employment twelve months out of the year. Liberty also provides financing to franchisees that open franchisees, giving Liberty another revenue stream but also helping the company expand.

I was surprised to learn that the tax preparation market is so fragmented with H&R Block commanding the biggest share by a single company at 16%. Liberty's current share equals Jackson Hewitt's at 2% with private CPA practices commanding 15% and mom-and-pop shops making up the biggest share at 65%. Liberty is targeting the mom-and-pop segment for consolidation and there is a clear opportunity to do so. Liberty can offer financial products that mom-and-pop shops likely cannot, and Liberty can transform previous mom-and-pop tax preparers into Liberty franchises with their financial products and infrastructure.

Liberty Will Return to Growth

The total number of returns prepared by Liberty grew 3.7% on a compounding basis from 2011 to 2015, outpacing the growth of all returns. Further, revenue in Liberty offices grew 6.5% on a compounding basis over that same timeframe. Overall revenue grew 8.3% on a compounding basis from 2011 to 2015 but growth slowed in 2015 year-over-year to 1.3%:

Source: Liberty Tax Presentation (attached)

To increase growth and take advantage of changing demographics, Liberty launched 'SiempreTax+' in 2015 to attract Spanish-speaking taxpayers. The Hispanic population in the U.S. is expected to be 19% in 2020, up from 16% in 2010 and reaching 22% in 2030. Thus, Liberty has an opportunity to benefit from a growing market with unique needs. SiempreTax+ is an independent brand under Liberty and offers assistance in getting driver's licenses, establishing residency, and also offers immigration services in addition to tax preparation. The number of SiempreTax+ locations grew 153% to 144 locations after a year from launch; in addition to SiempreTax+, Liberty has over 800 offices that can cater to Spanish speakers.

Click to enlarge

Click to enlarge

Source: Liberty Tax Presentation (attached)

Recent Results

Liberty's stock is down 45% over the last twelve months and that is even after a 21% rally in the last three months. The company reported results for its 2016 fiscal year in mid-June with revenue increasing 7% to $173.4 million and GAAP and non-GAAP EPS increasing 126% and 4%, respectively, to $1.38 and $1.41.

The large deviation in the GAAP and non-GAAP results was a result of litigation and impairment charges in 2015. Liberty incurred a litigation charge that reduced EPS by $0.33; the litigation charges stemmed from settlements of class action lawsuits related to Liberty's electronic refund checks (ERCs) for taxpayers and its auto-dialing practices. More information on these suits can be found on F-35 in the 2015 annual report that is attached. The important takeaway here is that the charges have been recognized and will not reoccur as evidenced in 2016. The impairment charges were related to the impairment of software for Liberty's online tax preparation services and the customer lists from the online business. The company's investment in software and foray into the online market was not as successful as planned; Liberty has written down its software and customer lists as a result and will concentrate on the brick-and-mortar business instead of the DIY market online. More on these impairments charges can be found starting with F-19 in the 2015 annual report.

Turning back to 2016, the fall in Liberty's stock price was precipitated by less than stellar results in 2016. The total number of returns filed in offices (excludes online filings) declined 3.8% to 2.16 million in the U.S. and Canada. The surprising revenue increase in light of this was driven by 22% growth in financial products, particularly in refund advances. People want their refunds quickly and Liberty can benefit from continuing to offer refund advances. What's good about refund advances is that there is little to no credit risk as the government is paying the refunds. Tax preparation fees also increased mightily by 39% as a result of an increase in company-owned locations from 182 to 310. The average net fee also grew 5.1% for tax preparation, so this aided the increase in revenue as well. Liberty captures the entire fee in this instance as opposed to a franchise fee with non-company-owned locations. I expect the fee per preparation to grow as filings become more complicated as discussed earlier.

Here is the summary of Liberty's results year-over-year and the reconciliations between the GAAP and non-GAAP results:

The Opportunity

Liberty no doubt has to increase the number of returns but the leverage from doing so is substantial given its success with its financial products and the growth in the average fee per filing. Liberty's targeting of the Hispanic market I believe will reward the company and its investors by leveraging not only a growing market but also a market that is not particularly familiar with the intricacies of the U.S. tax system and its growing complexity. Further, Liberty has a business model that can attract temporary employees and people looking to start their own businesses in an Uber-like fashion. I think this flexibility will allow it to attract further franchisees and allow it to return to growth in the number of returns filed.

On the financial side, Liberty remains a well-capitalized company with a debt-to-equity ratio of only 0.16 and a current ratio of 2. These measures are in line with where they have been for Liberty historically. Liberty has been cash flow positive and now pays a dividend of $0.64 per share, equating to a 4.7% yield - a sign that the company is confident in its financial strength and ability to generate cash.

Looking at valuation, Liberty now trades at a P/E of 10 compared to 16 for H&R Block; 28 for the larger industry; and 20 for the S&P 500 according to Morningstar. Likewise, Liberty trades at a discount compared to the three on a P/CF (operating cash flow) basis with a P/CF of 6; H&R Block carries a P/CF of 11; the industry 12; and the S&P 500 13 according to Morningstar. Turning back to P/E, Liberty has not traded this low since 2012 and its P/E has been 20 to 30 in previous years. Liberty has taken a hit because of the decline in returns, but revenue has still increased and there is significant operational leverage to squeeze more profits out of every return filed.

Another positive for Liberty is that its stock is significantly held by insiders, particularly its founder, CEO, and chairman, John T. Hewitt. Key insiders hold 14.5% of Liberty's outstanding shares and Hewitt holds most of them by owning 12.3% of Liberty's shares. Thus, Hewitt and other insiders are well-incentivized to see Liberty's share price rebound and could even be enticed to buy out the company if the share price lagged for a long period of time at a low valuation. Liberty Director, Robert M. Howard, has made the most significant transactions as of late with outright purchases of Liberty stock in the last two months; Howard has purchased 27,000 Liberty shares at prices ranging from $12.25 - $13.25, amounting to close to $350,000 worth of Liberty shares at the average of the range.

Insiders seem to not have turned their back on Liberty and the stock trades at a discount to itself historically and compared to competitors and the market. Still, there are risks and they could materialize in tax reform with the election of a new president. It seems tax reform and simplifying the tax code is always an issue but it never gets done. If there were some tax reform that simplified the tax code, then that could materially affect the need for educated preparers and decrease the fees charged per filing. It may even lead to more people doing their own taxes if filing became simpler. Another risk to Liberty's results could materialize from raises in the minimum wage; many of Liberty's employees are seasonal and earn a wage at or near minimum, so an increase to say $15 per hour could add significantly to Liberty's cost base. At the current valuation, however, I believe Liberty presents a good reward profile given the risk.

Liberty generated ROE of 17% in 2016 and excluding 2015 ROE of 8% due to the onetime charges and the highest ROE of 23% in 2014, ROE has averaged 18% since 2010. Using current shareholders' equity of $111.5 million, a forecast for income of $20 million and EPS of $1.43 with current diluted shares outstanding of 13,967,568 is achieved. The potential upside is outlined at the current price and the previous forecasted EPS at various P/E multiples:

SiempreTax+ should help Liberty return to growth in the number of tax filings and not just revenue. The tax environment should play to Liberty's favor. The company just has to execute on attracting mom-and-pops to convert and opening new Liberty offices. Still, financial products will play a major part in Liberty's success going forward. I think Liberty's share price can return to upwards of $20 with a return to growth, and the stock offers significant upside with the risks and past results already baked in.

Disclosure:I/we have no positions in any stocks mentioned, but may initiate a long position in TAX over the next 72 hours.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.